How AI in Finance Is Reshaping Risk, Lending, and Fraud Detection

The global AI in finance market was valued at $9.45 billion in 2023 and is projected to reach $44.08 billion by 2030, growing at a compound annual growth rate of nearly 25%. That trajectory is not a forecast built on optimism. It reflects spending that is already committed, pilots that have already converted into production systems, and competitive gaps that are already widening between institutions that adopted early and those still evaluating. The financial sector's total spending on artificial intelligence is expected to climb from $35 billion in 2023 to $97 billion by 2027, making finance one of the largest single industry investors in AI globally.

Yet the adoption picture is far from uniform. According to a 2026 Cambridge Centre for Alternative Finance report, 81% of surveyed financial services firms are adopting AI at some level, but only 14% currently view AI as transformational to their organisational strategy. That gap between experimentation and strategic integration is the central challenge facing every bank, insurer, asset manager, and fintech today. Institutions that close it will define the next decade of financial services. Those that do not will find themselves competing on cost alone, without the analytical edge that modern markets demand.

This blog examines exactly how AI in finance is changing the competitive landscape, from fraud detection and credit risk to portfolio management and regulatory compliance. It provides specific data on what early adopters are achieving, a practical roadmap for implementation, an honest assessment of the obstacles, and a forward view of where the industry is heading by 2030. Whether you are a CFO weighing your first AI investment or a CTO scaling your second generation of models, the information here is built to support real decisions.

The Current State of Finance: Pressure From Every Direction

The financial services industry in 2026 operates under a set of pressures that would have been difficult to imagine even five years ago. Interest rate volatility, compressed margins, rising regulatory scrutiny, and the rapid expansion of fintech competitors have created an environment where operational efficiency is no longer a strategic advantage. It is a survival requirement.

Consider the lending sector. Auto loan delinquencies have surged to their highest levels since the 2008 recession, signalling emerging vulnerabilities across the broader credit market. Traditional credit scoring models, built on static data snapshots, cannot reflect a borrower's changing financial health in real time. A consumer who was creditworthy at origination may show signs of distress within months, but legacy systems often fail to detect those signals until a payment is already missed. This creates a blind spot that costs lenders billions annually in charge offs and recovery expenses.

Fraud is an equally severe and accelerating problem. In 2024, US consumers lost over $12.5 billion to fraud schemes, nearly four times the $3.5 billion lost just four years earlier in 2020. Deepfake fraud cases surged by 1,740% in North America between 2022 and 2023, with financial losses exceeding $200 million in the first quarter of 2025 alone. Rule based detection systems that rely on static thresholds are overwhelmed by the speed, scale, and sophistication of modern fraud. The cost of inaction compounds every quarter.

On the regulatory front, compliance teams are managing an expanding set of obligations across jurisdictions. Anti money laundering requirements, consumer data protections, fair lending mandates, and emerging AI governance frameworks all demand resources that most institutions struggle to allocate. Manual compliance processes are slow, expensive, and prone to the kind of human error that invites enforcement action. The institutions that continue to rely on spreadsheet driven compliance risk both financial penalties and reputational damage.

Meanwhile, customer expectations have shifted permanently. Consumers who experience instant, personalised service from technology companies expect the same from their bank or insurer. A three day loan approval process feels antiquated when a fintech competitor can deliver a decision in minutes. This expectation gap is not theoretical. It is driving customer attrition at traditional institutions and fuelling the growth of digital first alternatives that were built from the ground up on data driven architectures.

How AI in Finance Is Transforming Core Operations

The transformation underway is not a single technology applied uniformly. It is a set of distinct AI capabilities, each mapped to a specific operational challenge. Understanding which technology solves which problem is essential for any institution evaluating its AI strategy.

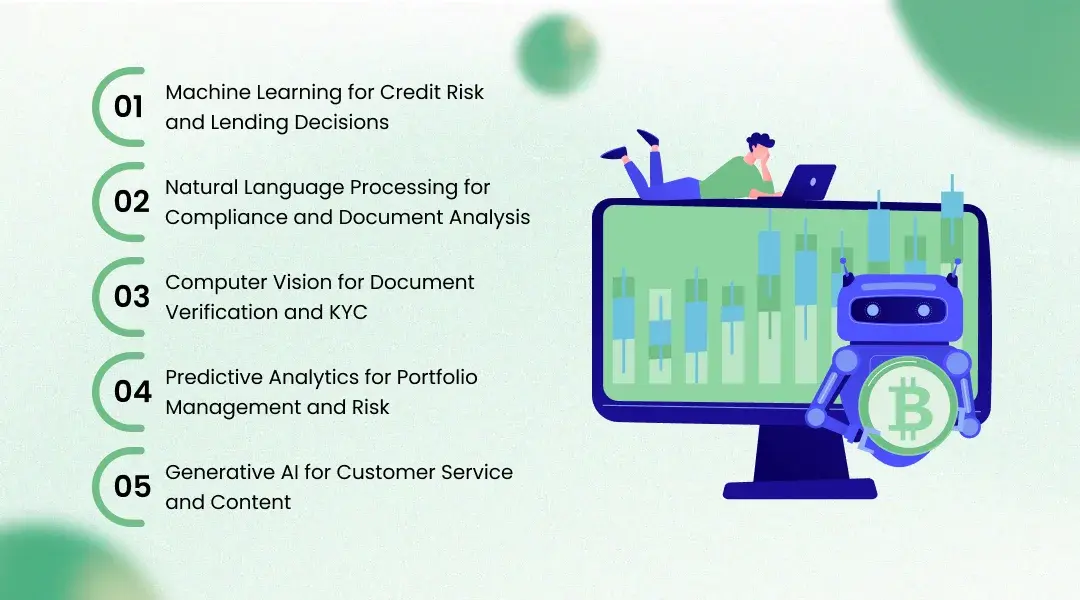

Machine Learning for Credit Risk and Lending Decisions

Machine learning models are fundamentally changing how lenders assess creditworthiness. Unlike traditional scorecards that rely on a handful of static variables, ML models can ingest hundreds of data points including transaction patterns, cash flow trends, employment stability signals, and alternative data sources such as utility payment histories. Financial institutions using AI powered credit assessment report up to 20% lower default rates compared to traditional methods. This improvement stems from the models' ability to detect non linear relationships between variables that statistical regression simply cannot capture.

JPMorgan Chase, for instance, uses machine learning to analyse cash flow data for small business loans, enabling faster and more accurate lending decisions. The practical impact extends beyond accuracy. AI driven underwriting reduces decision times from days to minutes, allowing lenders to process higher volumes without proportional increases in headcount. For borrowers, particularly those with thin credit files or non traditional income sources, ML models can unlock access to credit that conventional systems would deny. KriraAI works with financial institutions to build precisely these kinds of adaptive credit models, designed to integrate with existing loan origination systems and produce explainable risk scores that satisfy both business and regulatory requirements.

Natural Language Processing for Compliance and Document Analysis

Regulatory compliance generates enormous volumes of unstructured text, from new regulatory publications and legal opinions to internal audit reports and customer correspondence. Natural language processing models can now parse, classify, and extract actionable insights from these documents at a speed and scale that human analysts cannot match. NLP is being applied to automate suspicious activity report drafting, to monitor regulatory changes across jurisdictions, and to extract key terms from loan agreements for portfolio level analysis.

The compliance application is particularly valuable because the cost of getting it wrong is so high. A missed regulatory update or an improperly filed report can trigger fines that dwarf the cost of any technology investment. NLP systems do not eliminate the need for compliance professionals, but they shift those professionals from manual document review to higher value oversight and decision making.

Computer Vision for Document Verification and KYC

Know Your Customer processes remain one of the most resource intensive operations in financial services. Computer vision models can now verify identity documents, detect forgeries, match facial images, and extract data from scanned forms with accuracy rates that exceed manual review. These capabilities are especially important as synthetic identity fraud grows. Fraudsters are creating increasingly sophisticated fake documents, and rule based verification systems lack the pattern recognition capability to catch them consistently.

Predictive Analytics for Portfolio Management and Risk

Predictive analytics represents the most mature AI application in finance. Portfolio managers use predictive models to forecast asset price movements, assess tail risks, and optimise allocation strategies. Risk management teams deploy ensemble models that combine market data, macroeconomic indicators, and firm specific signals to generate early warning systems for portfolio stress. AI driven trading desks achieve roughly 10% higher risk adjusted returns as measured by Sharpe ratios, and risk models with AI integration allow firms to reduce capital reserves by approximately 12% while maintaining the same risk thresholds.

Generative AI for Customer Service and Content

Generative AI has moved beyond the hype cycle and into production at major financial institutions. Customer facing chatbots powered by large language models can handle complex queries about account balances, transaction disputes, loan terms, and product recommendations without human intervention. Banks using AI powered customer service report a 20% increase in customer satisfaction scores. Behind the scenes, generative AI is being used to draft internal reports, summarise research, and produce personalised marketing content, tasks that previously required significant analyst time.

Quantified Business Impact: What the Numbers Show

The business case for AI in finance is no longer speculative. It is being measured across every major operational category, and the results consistently show returns that justify the investment within 12 to 18 months of deployment.

In fraud prevention, the numbers are striking. HSBC's AI system reduced false positives by 60% while detecting two to four times more suspicious activities, processing 1.35 billion transactions monthly. Danske Bank achieved a 60% reduction in false positives and a 50% increase in true fraud detection after replacing its rule based systems with machine learning. Across the industry, AI fraud detection in banking saves an estimated $5 billion annually in prevented losses. A network of 1,500 credit unions saved approximately $35 million in fraud losses over 18 months after implementing an AI driven detection platform.

Operational efficiency gains are equally compelling. AI automates approximately 45% of back office tasks in banking, freeing an average of 1.5 full time equivalents per branch. That translates directly to cost savings that can be reinvested in growth initiatives or passed through to improved margins. AI reduces operational costs in finance by 30% on average across institutions that have moved beyond pilot stage. For fintech companies, AI adoption has boosted revenue per employee by 25%, a metric that reflects both the automation of routine tasks and the ability to serve more customers per agent.

In lending, the impact shows up in portfolio quality. Institutions using predictive analytics for lending report measurably lower default rates and faster time to decision. Personalised AI recommendations increase cross sell rates by 35%, meaning that existing customer relationships generate more revenue without proportional increases in acquisition cost. Insurers that have deployed AI in underwriting have cut claims processing time by 50%, a change that improves both operational efficiency and customer experience.

These are not projections. They are results being reported by institutions that have committed to AI as a core operational capability rather than a peripheral experiment. The gap between AI adopters and non adopters is widening every quarter, and the cost of delay compounds in ways that many executives underestimate.

The AI Implementation Roadmap for Financial Institutions

Implementing AI in a financial institution is fundamentally different from implementing it in most other industries. The regulatory environment is stricter, the data sensitivity is higher, the tolerance for error is lower, and the legacy technology landscape is more complex. A disciplined, staged approach is essential.

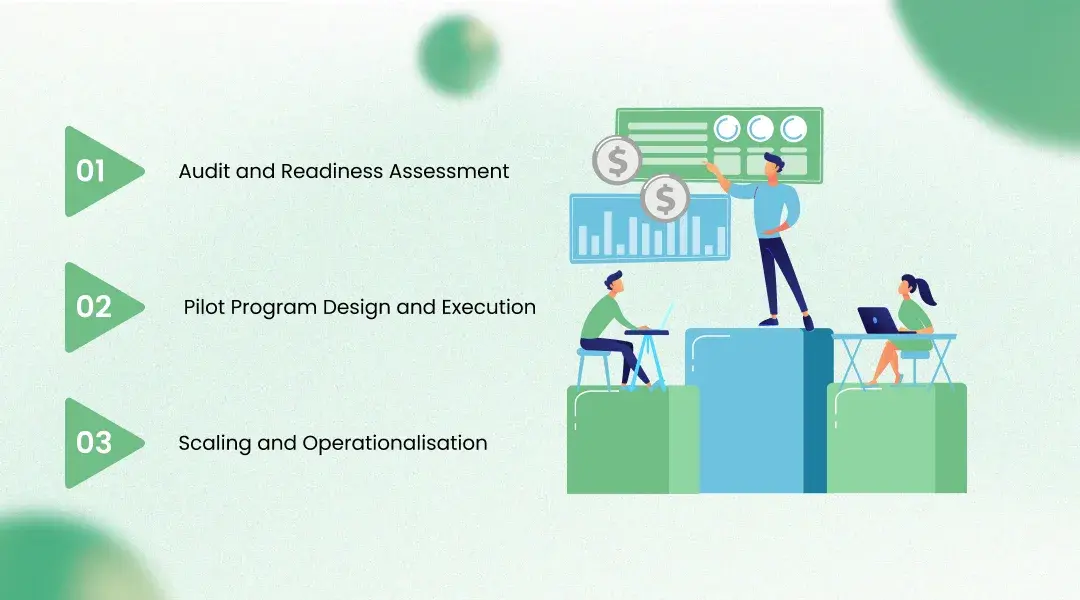

Phase One: Audit and Readiness Assessment

Before any AI investment, an institution must understand its current data infrastructure, talent capabilities, and process maturity. This assessment should answer several critical questions:

What data assets does the organisation actually have, and what is their quality, completeness, and accessibility?

Where are the highest value use cases, meaning the processes where AI can deliver the largest measurable impact in the shortest time?

What regulatory constraints apply to the specific use cases being considered, and what explainability requirements must the models meet?

What is the current state of the technology stack, and what integration work will be required to operationalise AI models?

This phase typically takes six to twelve weeks and should produce a prioritised list of use cases ranked by feasibility, impact, and risk. KriraAI typically begins client engagements at this stage, conducting data audits and process mapping exercises that identify the two or three highest return AI applications for each institution's specific operating model.

Phase Two: Pilot Program Design and Execution

The pilot phase should focus on a single, well defined use case with clear success metrics. For most financial institutions, fraud detection or credit risk scoring are ideal starting points because they have measurable baselines, large datasets, and direct revenue impact. A successful pilot typically runs for three to six months and should demonstrate not only model performance but also operational integration, meaning the model's outputs are actually being used in live decision processes.

Key pilot design principles include defining success metrics before the pilot begins, using production quality data rather than sanitised test sets, involving front line users in the design process to ensure the model's outputs are actionable, and establishing a model governance framework from day one rather than retrofitting it later.

Phase Three: Scaling and Operationalisation

Moving from pilot to production is where most AI initiatives stall. The technical challenges of scaling, including model monitoring, retraining pipelines, latency requirements, and failover systems, are significant. But the organisational challenges are often harder. Business units may resist changes to established workflows. Risk committees may demand levels of explainability that constrain model complexity. IT teams may lack the infrastructure to serve models at the required throughput.

Successful scaling requires executive sponsorship that extends beyond the initial champion. It requires cross functional governance that includes risk, compliance, technology, and business stakeholders. And it requires a clear communication strategy that helps front line staff understand what the AI does, what it does not do, and how their role evolves alongside it.

Common Mistakes and How to Avoid Them

The most damaging mistakes in AI implementation are rarely technical. They are strategic and organisational.

Starting with too many use cases simultaneously, which dilutes focus and stretches limited data science talent across too many workstreams.

Treating AI as a technology project rather than a business transformation, which results in models that work technically but never get adopted operationally.

Neglecting data quality in favour of model sophistication, which produces impressive demos that fail in production because the input data is inconsistent, incomplete, or biased.

Failing to establish model risk management frameworks before deployment, which creates regulatory exposure that can force a programme to shut down entirely.

Underinvesting in change management, particularly training for front line staff who must learn to trust and act on model outputs.

Each of these mistakes is avoidable with proper planning and experienced guidance. The institutions that succeed are those that treat AI implementation as a multi year strategic programme, not a one off technology purchase.

Challenges and Limitations of AI in Financial Services

Honest assessment of AI's limitations is essential for any institution considering adoption. The technology is powerful, but it is not without significant constraints that must be managed carefully.

Data quality remains the single largest obstacle. Financial institutions typically operate with data spread across dozens of legacy systems, many of which use incompatible formats, inconsistent naming conventions, and incomplete records. AI models are only as good as the data they consume, and building the data pipelines required to feed production models is often more expensive and time consuming than building the models themselves. Institutions that skip the data engineering work in favour of rushing to model development consistently underperform.

The talent gap is real and persistent. Despite growing interest in AI careers, the supply of professionals who combine deep machine learning expertise with financial domain knowledge remains limited. Hiring a strong data scientist is difficult. Hiring one who also understands credit risk modelling, regulatory requirements, and the operational realities of a bank is substantially harder. This scarcity drives up costs and creates retention challenges that can destabilise AI programmes.

Regulatory uncertainty adds another layer of complexity. Global AI regulations for finance are expected across 80% of jurisdictions by 2026, but the specific requirements vary significantly by region. The European Union's AI Act imposes strict transparency and explainability requirements on high risk AI applications, a category that includes credit scoring and fraud detection. US regulators are taking a more sector specific approach, with different agencies issuing overlapping and sometimes conflicting guidance. Institutions operating across borders must navigate this patchwork of requirements, which increases both the cost and the complexity of deployment.

Integration with legacy systems is a persistent technical challenge. Many financial institutions run core banking platforms that are decades old, built on technologies that were never designed to interact with modern AI infrastructure. Connecting a real time machine learning model to a mainframe based transaction processing system requires middleware, API layers, and data transformation logic that can take months to build and test. Gartner predicts that more than 40% of agentic AI projects will be cancelled by the end of 2027 due to rising costs and unclear business outcomes, a statistic that reflects the difficulty of translating promising technology into operational reality.

Finally, bias and fairness concerns demand ongoing attention. AI models trained on historical financial data can perpetuate and even amplify existing biases in lending, insurance, and other decision processes. The Apple Card credit limit controversy, in which the algorithm was accused of assigning lower limits to women, demonstrated how quickly a bias issue can escalate into a public relations and regulatory crisis. Institutions must invest in bias testing, model auditing, and fairness metrics as core components of their AI governance framework, not as afterthoughts.

The Future of AI in Financial Services: 2026 to 2030

The next three to five years will bring changes to financial services that are more structural than anything the industry has experienced since the introduction of electronic trading. Three developments in particular will reshape the competitive landscape.

Agentic AI is the most significant near term shift. Unlike traditional AI systems that respond to queries or score transactions, agentic AI systems can autonomously execute multi step workflows, make decisions within defined parameters, and interact with other systems without human intervention. In early 2026, 52% of financial services firms are already in active adoption of agentic AI. By 2028, agentic AI is projected to generate up to $450 billion in economic value globally through revenue uplift and cost savings. In finance specifically, agentic systems will handle end to end loan processing, continuous compliance monitoring, autonomous portfolio rebalancing, and real time fraud response. The institutions that deploy these systems effectively will operate with fundamentally different cost structures than those that do not.

The convergence of AI with real time data infrastructure will enable capabilities that are currently impossible. Today, most AI models in finance operate on batch processed data that is hours or days old. As financial institutions migrate to streaming data architectures, AI models will operate on live transaction flows, market feeds, and customer interaction data simultaneously. This shift will make truly predictive operations possible, where institutions can identify and respond to risks, opportunities, and customer needs before they fully materialise. KriraAI is already building solutions for this real time AI paradigm, working with financial institutions to architect the data infrastructure and model serving layers required for sub second decision making at scale.

The competitive gap between AI leaders and laggards will become irreversible. Fintechs already lead traditional financial institutions by 47% to 30% in advanced AI adoption, and 19% of fintechs have reached a transforming stage of adoption compared to just 6% of incumbents. As AI capabilities compound over time, through better models, more data, and deeper operational integration, the advantage held by early adopters will become increasingly difficult for late movers to close. Institutions that have not established a serious AI strategy by 2027 will find themselves competing against organisations that can underwrite loans faster, detect fraud earlier, serve customers more effectively, and manage risk more precisely at every level of operation.

Conclusion

Three core insights emerge from this analysis of AI in finance. First, the technology has moved decisively beyond experimentation. Institutions deploying AI in fraud detection, lending, and risk management are achieving measurable results, including 50% to 60% reductions in false positive rates, 20% lower default rates, and 30% average reductions in operational costs. Second, successful implementation requires a disciplined, staged approach that prioritises data quality, regulatory compliance, and organisational change management over model sophistication. Third, the competitive window for establishing an AI advantage is narrowing rapidly, as fintechs and forward looking incumbents build compounding advantages that late movers will struggle to replicate.

For financial institutions ready to move from evaluation to execution, the critical first step is an honest assessment of current capabilities and a clear identification of high value use cases. KriraAI partners with banks, insurers, and financial services firms to conduct exactly this kind of strategic assessment, followed by the design and deployment of AI solutions built for the specific regulatory, operational, and data realities of each institution. From predictive credit models and AI risk management financial services platforms to real time fraud detection systems, KriraAI delivers solutions that are practical, measurable, and engineered for production scale. If your institution is ready to close the gap between AI potential and operational reality, explore how KriraAI can help you build the foundation for what comes next.

FAQs

The optimal timing for an AI voice agent to initiate a cart recovery call is between 5 and 30 minutes after the abandonment event. Calling within this window catches the shopper while they still have active purchase intent and can recall the specific items they were considering. Research on sales response timing consistently shows that contact within the first five minutes produces the highest conversion rates, but the practical sweet spot for cart recovery is typically 15 to 20 minutes, which allows enough time for the shopper to have genuinely abandoned rather than simply pausing during checkout. Calling too quickly, within one to two minutes, can feel intrusive and suggests surveillance. Calling too late, after several hours or the next day, produces results only marginally better than email. AI voice agent platforms like OnDial allow businesses to configure precise timing rules based on their customer behaviour data, including different timing for different cart values, product categories, or customer segments.

Customer reception of AI cart recovery calls depends entirely on execution quality. Poorly designed calls with robotic voices, aggressive scripts, or irrelevant offers do generate negative reactions and can damage brand perception. However, well-designed AI voice interactions that sound natural, reference the specific products the customer was considering, and offer genuine value such as addressing a concern or providing a relevant incentive are received positively by the majority of shoppers. Studies on consumer attitudes toward proactive customer service consistently show that 60% to 70% of consumers appreciate follow-up contact from brands they were actively shopping with, provided the contact is timely, relevant, and respectful. The key factors are voice quality, conversation naturalness, the ability to handle "not interested" gracefully, and compliance with calling regulations and consent requirements. OnDial's platform is built with GDPR and CCPA compliance as foundational requirements, ensuring that all recovery calls meet regulatory standards for consent and data handling.

E-commerce businesses deploying AI voice agents for cart recovery can realistically expect to recover between 15% and 25% of abandoned carts, depending on factors including product category, average order value, conversation design quality, call timing, and whether incentives such as discounts or free shipping are offered during the recovery call. This compares favourably to email recovery rates of 5% to 10% and SMS recovery rates of 10% to 15%. Higher-value carts tend to show higher recovery rates because customers who have invested more time in product selection are more receptive to a conversation that addresses their specific hesitation. The first month of deployment typically shows recovery rates at the lower end of this range as the conversation flows are optimised, with performance improving steadily as the AI agent's objection handling is refined based on real call data and sentiment analysis.

Yes, modern AI voice agent platforms support multilingual cart recovery, which is essential for e-commerce businesses serving diverse markets. The AI agent can detect the customer's preferred language based on their profile data, browser language settings, or previous interaction history, and conduct the entire recovery conversation in that language. This capability is particularly important for e-commerce businesses operating in multilingual markets such as India, where a single store might serve customers who prefer Hindi, Tamil, Bengali, Telugu, or English. OnDial supports over 100 languages and offers more than 80 Indian voice variations across 9 Indian languages, enabling e-commerce businesses to deploy recovery agents that communicate fluently in the customer's native language without maintaining separate agent teams for each language.

AI voice agents for abandoned cart recovery work most effectively as part of an orchestrated multi-channel recovery strategy rather than as a replacement for email and SMS. The recommended approach is to position the AI voice call as the first recovery touchpoint, initiated within 15 to 30 minutes of abandonment, followed by email and SMS sequences for carts that the voice agent did not recover. This sequencing leverages the voice channel's higher conversion rate for the initial, highest-intent window while using email and SMS as lower-cost follow-up channels for shoppers who were unreachable by phone or who need more time to decide. The integration requires coordination between the AI voice platform and the e-commerce platform's marketing automation system, typically managed through shared cart status data that prevents a shopper from receiving a recovery email for a cart that was already recovered via a voice call. OnDial's API integration enables this orchestration by updating cart and customer status in real time as recovery calls are completed.

Founder & CEO

Divyang Mandani is the CEO of KriraAI, driving innovative AI and IT solutions with a focus on transformative technology, ethical AI, and impactful digital strategies for businesses worldwide.