AI in Finance: Why Adoption Isn't the Same as Advantage

Eighty one percent of financial services firms are now using AI in some form, yet only fourteen percent of those same firms believe it has actually become transformational to their strategy or competitive position. That gap, between near universal adoption and rare strategic payoff, is the most important and least discussed story in financial technology right now. Most coverage of AI in finance still asks whether banks and lenders should adopt the technology, as if that question were unresolved. It is resolved. The real question, the one boards and CFOs are quietly struggling with, is why so much investment is producing so little transformation.

This is not a story about AI failing to work. Fraud detection models at major banks are intercepting fraudulent transactions with accuracy rates above ninety percent, document processing times have collapsed from days to minutes, and generative AI tools are drafting compliance reports that used to consume entire analyst teams. The technology is delivering. What is missing, in the large majority of institutions, is the organizational discipline to turn isolated wins into compounding advantage. Four of the five most common AI use cases in financial services today are back office functions, which tells its own story about ambition versus impact.

This blog breaks down where the financial industry actually stands today, which AI technologies are doing the real work behind the headlines, what the quantified returns look like when implementation is done correctly, and how a realistic roadmap should be sequenced. It also covers the failure points nobody wants to put in a press release, and where the competitive landscape is heading over the next several years. By the end, the gap between adopting AI and actually benefiting from it should be far less mysterious.

The State of Financial Services Before the AI Conversation Even Starts

Financial services has always been an industry defined by paradox. It is simultaneously one of the most profitable sectors in the global economy and one of the most operationally burdened, carrying decades of legacy infrastructure, fragmented data systems, and compliance obligations that grow heavier every year. Most large banks still run core systems built on mainframe architecture from the 1970s and 1980s, patched repeatedly rather than replaced, because replacement carries existential risk if something breaks mid migration. This technical debt is not a minor inconvenience. It is the primary reason that innovation in finance has historically moved slower than in almost any other knowledge industry.

Cost pressure compounds the problem. Net interest margins have been squeezed for years by competitive pricing and rate volatility, while customer acquisition costs in retail banking and lending continue to climb as digital-first challengers fragment the market. Compliance costs alone consume a significant share of operating budgets at most mid sized and large institutions, driven by anti money laundering requirements, know your customer obligations, and an expanding patchwork of regional and international regulation. A single regulatory exam can require months of document preparation, and the cost of getting it wrong, in fines, reputational damage, or both, has only grown more severe in recent years.

Labor dynamics add another layer of strain. Financial institutions have historically solved operational scaling problems by hiring more analysts, more underwriters, and more compliance officers, but that model breaks down when transaction volumes and fraud sophistication grow faster than headcount budgets allow. At the same time, customer expectations have shifted permanently. People who can get a same day answer from a retailer or a same hour resolution from a tech company are far less patient with a five day loan decision or a hold music compliance call. The competitive set has also widened, with fintech challengers, embedded finance providers, and even large technology companies entering lending, payments, and wealth management with structurally lower cost bases. None of this required AI to become a problem. AI is simply the tool now available to address a set of pressures that were already mounting well before generative models or machine learning entered the conversation.

How AI Is Transforming Finance: The Technologies Behind the Headlines

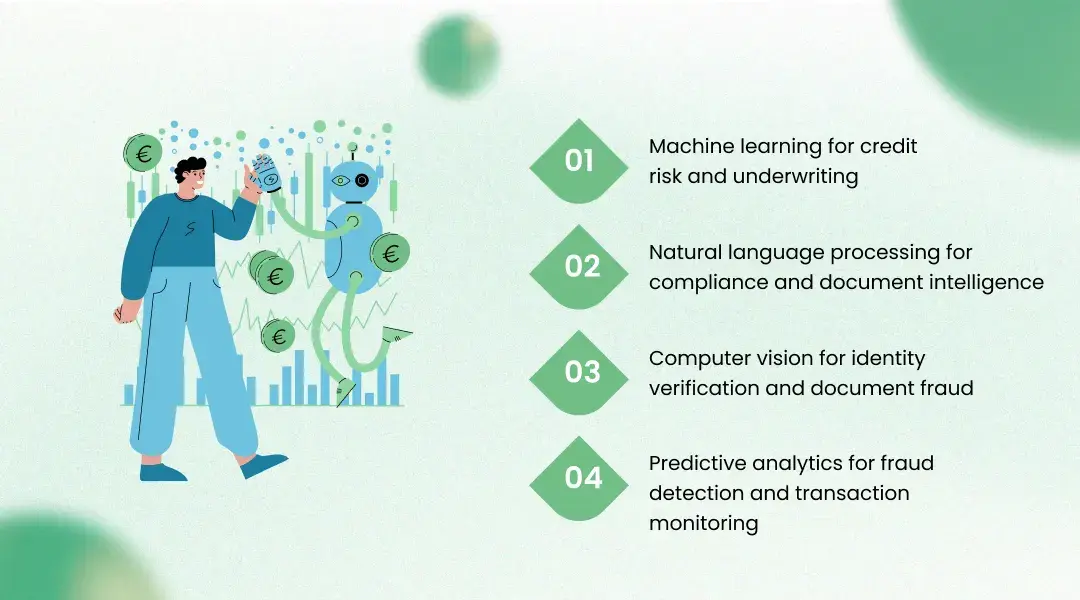

Most coverage of artificial intelligence in financial services treats it as a single monolithic force, which obscures what is actually happening. In practice, at least five distinct categories of AI technology are doing very different jobs, and mapping the right technology to the right problem is the difference between a pilot that scales and one that quietly dies after six months.

Machine learning for credit risk and underwriting

Machine learning models, particularly gradient boosted decision trees and ensemble methods, have replaced or augmented traditional credit scoring in a growing share of lending operations. Unlike legacy scorecards built on a handful of static variables, these models can ingest hundreds of signals, including transaction patterns, cash flow volatility, and alternative data sources, to produce risk assessments that update continuously rather than at quarterly intervals. This matters most for thin file borrowers, small businesses, and emerging market customers who were historically underserved by rigid scoring criteria built around decades old assumptions about creditworthiness.

Natural language processing for compliance and document intelligence

Natural language processing is now doing work that used to require entire teams of paralegals and compliance analysts. Contract review, regulatory filing analysis, and adverse media screening for anti money laundering checks have all moved from manual reading to automated extraction and classification. Document intelligence systems can pull structured data out of loan applications, KYC documentation, and trade confirmations in formats that previously required manual rekeying, cutting processing time from days to minutes in well implemented deployments.

Computer vision for identity verification and document fraud

Computer vision plays a quieter but increasingly critical role, primarily in identity verification and document authentication. When a customer opens an account remotely and submits a photo of a government ID alongside a selfie, computer vision models are checking for tampering, verifying liveness to prevent deepfake based spoofing, and cross referencing facial features against the submitted document in real time. As deepfake fraud attempts have surged, this layer of defense has become non negotiable rather than optional for any institution offering digital onboarding.

Predictive analytics for fraud detection and transaction monitoring

Predictive analytics, built on supervised and unsupervised learning models, now sits at the center of real time fraud detection. These systems analyze thousands of behavioral signals per transaction, including device fingerprinting, typing cadence, geolocation consistency, and historical spending patterns, scoring each transaction in milliseconds before it clears. Unlike static rule based systems that simply flag transactions exceeding a threshold, these models learn from confirmed fraud outcomes and analyst feedback, continuously recalibrating what looks suspicious as fraud tactics evolve.

Generative AI and agentic AI for customer service and workflow automation

Generative AI has moved fastest in customer facing and internal productivity applications. Conversational assistants are now handling a meaningful share of routine customer service inquiries, freeing human agents for complex cases that require judgment. More significantly, agentic AI, which can take multi step actions rather than simply generating text, is starting to automate entire workflows such as reconciliation, exception handling in payments processing, and first draft regulatory reporting. Industry researchers expect agentic AI to be the clearest growth frontier in financial AI through the rest of this decade, in large part because it requires lower technical integration effort than building custom machine learning pipelines from scratch.

The technologies above are not competing with each other. They are complementary layers, and the institutions seeing real transformation are the ones combining several of them around a single business problem rather than deploying each in isolation. A fraud detection program that uses predictive analytics for transaction scoring but never integrates natural language processing for case narrative writing is leaving obvious efficiency on the table.

The Quantified Business Impact: What Real Returns Actually Look Like

Vague claims about AI delivering value are easy to find and largely useless. What matters is what the numbers actually show when implementation is done well, and the data from real deployments paints a far more specific and credible picture than most marketing material suggests.

Fraud detection delivers some of the most mature and well documented returns in the entire industry. Machine learning based fraud systems have been shown to reduce undetected fraudulent transactions by roughly forty percent compared with rule based systems, while also cutting false positive rates significantly, in some documented cases by as much as sixty to ninety percent depending on the institution and the maturity of the deployment. JPMorgan Chase has reported a twenty percent reduction in false positive fraud cases, which translates directly into fewer legitimate customers having their cards declined and fewer analyst hours wasted chasing dead ends. HSBC has reported a sixty percent reduction in false positives following the rollout of its AI driven risk assessment system, a result that compounds over time as the model continues learning from analyst feedback.

The compliance and anti money laundering side of the business shows similarly concrete gains. Alert volume reductions of forty to sixty percent are commonly reported once institutions deploy better initial risk scoring that filters low risk activity before it ever reaches a human analyst's queue. Banks running automated anti money laundering workflows typically report spending thirty to forty percent less time preparing documentation for regulatory examinations, simply because the audit trail is structured automatically rather than assembled manually after the fact. These are not marginal efficiency gains. For a mid sized bank generating tens of thousands of fraud alerts annually, even a modest improvement in alert precision can translate into hundreds of thousands of dollars in annual savings, once analyst time and false positive customer friction are accounted for.

Document processing improvements tell a similarly compelling story. Institutions that have deployed document intelligence for loan origination and KYC processing report cutting document turnaround time from multiple days to a matter of minutes for the most routine cases, with exception handling for complex files still requiring human review but at dramatically reduced volume. Surveys of senior financial executives show that document intelligence and risk management now rank among the top use cases institutions are actively running or piloting, alongside data analysis and customer service automation, each cited by a majority of surveyed institutions as either fully running or in active pilot.

Even with this strength of evidence, the broader research is honest about a real measurement problem. Roughly three quarters of organizations report that their most advanced AI initiatives met or exceeded return on investment expectations, yet a much larger share of enterprises across industries still struggle to demonstrate clear business value from earlier, less mature generative AI experiments. This is not a contradiction. It reflects the difference between a narrowly scoped, well measured deployment, like fraud detection with a clear precision metric, and a broad, loosely defined generative AI rollout with no agreed definition of success from the outset. The lesson for any financial institution evaluating AI investment is straightforward: the use cases with the clearest, most measurable outcomes are consistently the ones generating the clearest, most defensible returns.

Implementation Roadmap: How Financial Institutions Should Actually Deploy AI

Most AI implementation failures in financial services are not technology failures. They are sequencing failures, where institutions skip foundational steps in pursuit of a visible win, and then discover months later that the foundation was never solid enough to support scale. A realistic roadmap looks substantially different from the version usually pitched in vendor sales decks.

Stage one is an honest readiness audit. Before any model gets built, the institution needs a clear inventory of its data quality, system architecture, and regulatory exposure for the specific function being targeted. This means identifying which data sources are clean enough to train a reliable model, which legacy systems will need integration work, and which compliance teams need to be involved from day one rather than brought in after the fact. Institutions that skip this stage almost always discover data quality problems midway through a pilot, at which point the timeline and budget have already been set against unrealistic assumptions.

Stage two is narrow, measurable pilot selection. The strongest pilots target a single, well bounded problem with an existing baseline metric, such as false positive rate in fraud alerts or average document processing time in loan origination. Trying to pilot something broad and strategic, like a generative AI assistant for the entire customer service organization, almost always produces ambiguous results because there is no clean baseline to measure against. A narrow pilot with a hard number attached is far more useful for building internal confidence and securing budget for the next phase.

Stage three is parallel running before full cutover. Any model touching fraud decisions, credit decisions, or compliance reporting should run in parallel alongside the existing system for a defined validation period before it is allowed to act independently. This is not bureaucratic caution. It is the only reliable way to catch a model's blind spots before those blind spots become customer facing incidents or regulatory findings.

Stage four is staged expansion with governance built in from the start. Once a pilot proves out, expansion should happen function by function rather than institution wide all at once, with model governance, explainability documentation, and a clear escalation path for edge cases established before each new function comes online. Institutions like KriraAI, which builds practical AI solutions for enterprises, typically structure this stage around a documented model risk framework precisely because regulators increasingly expect institutions to explain, not just defend, an AI driven decision.

Common Mistakes and How to Avoid Them

The same handful of mistakes recur across institutions of very different sizes and sophistication levels, and most of them are avoidable with earlier planning rather than additional technology spend.

Treating a pilot as a permanent solution is one of the most common errors, where a successful proof of concept never gets the additional engineering investment needed to handle full production volume and edge cases, so it stalls indefinitely in a perpetual pilot state. Underinvesting in change management is another frequent failure, since even a technically excellent model will be ignored or worked around by frontline staff if they were not involved in defining how it should be used. Choosing platforms based on vendor demos rather than explainability requirements creates serious problems later, because a model that cannot explain its decisions in plain language will eventually fail a regulatory examination regardless of how accurate it is. Underestimating data integration complexity is a near universal mistake, where institutions assume their data is cleaner and better connected than it actually is, only discovering the gaps once a model is already mid build. Finally, measuring success by adoption rate instead of business outcome leads institutions to celebrate the wrong milestone, declaring victory because a tool was deployed rather than because it actually moved a metric that mattered.

The Real Challenges Nobody Wants to Put in a Press Release

It would be dishonest to present AI in finance as a smooth, friction free path to transformation, because the honest reality involves several genuinely difficult and unresolved problems.

Data quality remains the single biggest practical obstacle inside most institutions. Decades of mergers, legacy system patches, and inconsistent data entry standards have left many banks with customer and transaction data that is fragmented across systems that were never designed to talk to each other. No AI model, regardless of sophistication, can compensate for training data that is incomplete, mislabeled, or simply wrong, and cleaning this data is often a multi year undertaking that competes for budget against more visible, headline grabbing AI initiatives.

The talent gap is equally real, though it manifests differently than most people assume. The scarce resource is not data scientists, of whom there is now a reasonably deep talent pool, but professionals who understand both the technical mechanics of machine learning and the regulatory, risk, and operational realities of financial services. A model built by a brilliant data scientist with no understanding of fair lending law or anti money laundering obligations is a regulatory incident waiting to happen, and institutions consistently underestimate how hard this hybrid skill set is to hire or build internally.

Regulatory uncertainty compounds the difficulty further. High risk AI use cases including credit scoring, fraud detection, and anti money laundering screening are increasingly subject to explainability requirements under emerging regulatory frameworks, with penalties for non compliance reaching as high as seven percent of global annual turnover under some proposed frameworks. Institutions building models today are effectively betting on how regulation will evolve over the next several years, and getting that bet wrong can mean rebuilding a production system from scratch.

Integration complexity and change management round out the list of genuine difficulties. Connecting a modern machine learning pipeline to a core banking system built decades ago is rarely as simple as an API call, and the organizational resistance from staff who fear the technology threatens their role can quietly sabotage even a technically sound deployment if leadership does not address it directly and early.

Where AI in Finance Is Headed Over the Next Three to Five Years

The trajectory of AI in financial services over the coming years points toward a level of autonomy and integration that goes well beyond what most institutions are running today. Agentic AI, capable of taking multi step actions rather than simply answering questions, is widely expected to become genuinely mainstream within financial workflows by around 2030, fundamentally changing how reconciliation, exception handling, and even portions of underwriting get executed without constant human initiation at every step. This is a meaningfully different model than the current generation of tools, most of which still require a human to prompt every action.

Personalization is likely to deepen substantially as institutions move past generic product recommendations toward genuinely individualized financial guidance generated in real time based on a customer's complete financial picture rather than a static segment they were assigned to years ago. Model governance and explainability will shift from a compliance afterthought to a competitive differentiator, since institutions that can clearly explain an AI driven credit or fraud decision to both regulators and customers will face fewer regulatory delays and build more durable customer trust than competitors still treating explainability as a checkbox exercise.

The competitive landscape will likely bifurcate further between fintech challengers and traditional incumbents, a gap that is already visible today given that fintechs report meaningfully higher rates of advanced AI adoption than traditional institutions. The institutions most likely to be left behind are not necessarily the ones with the least AI investment, but the ones that never moved past pilot stage deployments confined to back office functions, treating AI as a cost cutting tool rather than a foundation for new products and customer experiences. Investment levels alone will not determine the winners, since a meaningful share of institutions report relatively modest annual AI spending while still achieving high maturity in generative and agentic AI, suggesting that disciplined execution matters more than budget size. Companies like KriraAI are increasingly positioned to help bridge this exact gap, building AI systems specifically designed for the scale, governance, and explainability demands unique to regulated financial environments rather than repurposing generic enterprise software.

Conclusion

This is precisely the gap that KriraAI was built to close. Rather than offering generic enterprise software repackaged with an AI label, KriraAI works directly with financial institutions to design fraud detection, compliance automation, and document intelligence systems that are scoped around measurable outcomes from day one, with explainability and regulatory alignment built into the architecture rather than added afterward. For institutions that have already run a pilot or two but are struggling to translate early wins into organization wide advantage, that focus on practical, governed, scalable implementation is exactly where a partner like KriraAI tends to make the difference. If your institution is ready to move past experimentation and start building AI systems that hold up under regulatory scrutiny and deliver measurable returns at scale, reaching out to KriraAI is a sensible next step worth taking seriously.

FAQs

The biggest measurable benefit of AI in finance today is fraud detection and risk management, where institutions report false positive reductions ranging from twenty to ninety percent depending on deployment maturity, alongside detection accuracy improvements that allow genuine fraud to be caught in milliseconds rather than hours or days. Beyond fraud, document intelligence and compliance automation are delivering similarly concrete value, cutting document processing times from days to minutes and reducing regulatory examination preparation time by roughly thirty to forty percent at institutions with mature automated workflows. The common thread across every high performing use case is a clear, measurable baseline metric defined before deployment began, which is precisely what separates well documented returns from the vague generative AI experiments that struggle to demonstrate value.

Implementation cost varies enormously based on institution size, the specific use case, and whether the bank builds internally or partners with a specialist provider, but mid market transaction monitoring platforms typically run between eighty thousand and two hundred fifty thousand dollars annually on a cloud native, consumption based model. Legacy on premise alternatives can exceed five hundred thousand dollars annually once hosting, maintenance, and the developer hours required for ongoing rule tuning are factored in. Notably, more than half of surveyed financial institutions report spending under one hundred thousand dollars annually on AI overall while still achieving high maturity in generative and agentic AI, which suggests that disciplined, well scoped deployment matters considerably more than total budget size when it comes to achieving meaningful results.

AI in financial services is primarily automating specific tasks rather than eliminating entire roles outright, with the clearest impact concentrated in back office and routine processing functions such as document review, basic customer service inquiries, and initial fraud alert triage. Four of the top five current AI use cases in the industry are back office functions, which indicates that displacement, where it happens, is concentrated in repetitive processing work rather than judgment intensive roles like relationship management, complex underwriting, or regulatory strategy. The more accurate framing, supported by how institutions are actually deploying these tools, is that AI is shifting human attention toward higher value exception handling and complex cases while automating the high volume, low complexity work that previously consumed a disproportionate share of analyst time.

A first production deployment of AI fraud detection focused on alert triage, without full transaction blocking authority, can typically go live within ninety to one hundred twenty days, with a well calibrated model reaching alert precision rates of thirty five to fifty five percent within the first ninety days of operation, compared with the five to fifteen percent precision typical of older rule based systems. Extending the same system to real time transaction blocking rather than alert triage alone takes considerably longer, since it requires additional model validation, a formal governance review process, and in many jurisdictions a regulatory notification before deployment. Institutions should treat the ninety day mark as a realistic checkpoint for initial validated results rather than full strategic transformation, which typically takes considerably longer to materialize across the full fraud and compliance workflow.

AI adoption in finance refers simply to whether an institution is using AI tools at any level, a bar that the vast majority of the industry, around eighty one percent of surveyed firms, has already cleared. AI transformation refers to whether that AI usage has become genuinely strategic and central to competitive advantage rather than confined to isolated back office efficiency gains, a far higher bar that only about fourteen percent of surveyed institutions report actually reaching today. This gap exists because adoption requires购买ing or building a tool, while transformation requires redesigning workflows, governance structures, and sometimes entire product lines around what the technology makes newly possible, a much harder and slower organizational change that most institutions have not yet completed.

Three points matter more than any others when cutting through the noise around AI in finance. First, adoption is no longer the differentiator it once was, since the overwhelming majority of institutions are already using AI in some form, which means the real competitive battle has shifted to execution quality rather than mere presence of the technology. Second, the technologies generating the clearest, most defensible returns, fraud detection, document intelligence, and compliance automation, all share a common trait: a precise, measurable baseline defined before deployment, not after. Third, the institutions most at risk of falling behind over the next several years are not the ones spending the least on AI, but the ones that never moved past isolated back office pilots into governed, scaled, strategically integrated deployment.

Founder & CEO

Divyang Mandani is the CEO of KriraAI, driving innovative AI and IT solutions with a focus on transformative technology, ethical AI, and impactful digital strategies for businesses worldwide.