AI Implementation in Financial Services: What Actually Works

Global fraud losses on card payments alone crossed 33 billion dollars in recent industry estimates, and the curve is still bending upward. Banks are hiring compliance staff faster than revenue teams. A mid-sized lender now spends a meaningful share of operating costs simply proving to regulators that it followed its own rules. Against that backdrop, AI implementation in financial services has stopped being a strategic experiment and started behaving like basic infrastructure. The institutions pulling ahead are not the ones with the largest model budgets. They are the ones who picked narrow problems, measured them honestly, and rebuilt the plumbing underneath. Most of the sector is doing the opposite. It is running dozens of proofs of concept, celebrating demos, and shipping almost nothing into production. This blog examines why that gap exists, what the technology actually does inside a bank or insurer, what the returns look like when measured properly, how a serious rollout sequences itself, and where the competitive landscape moves next.

Finance Was Already Breaking Before AI Showed Up

The financial sector entered this decade carrying structural problems that no amount of headcount could solve. Margins on traditional lending compressed as capital became more expensive and competition arrived from outside the perimeter. Payment companies, retailers, and telecom operators began offering credit without carrying legacy branch networks. Meanwhile, the cost of simply staying legal kept climbing.

Compliance is the clearest example of a broken cost curve. Anti-money laundering programs at large institutions generate alert volumes where the overwhelming majority are false positives. Analysts spend their days clearing noise. Industry reporting has repeatedly placed false positive rates in transaction monitoring above ninety percent. Every one of those alerts still requires a human to close it.

Operations tells a similar story. Loan origination, claims handling, reconciliation, and client onboarding still depend heavily on documents. Those documents arrive as scans, emails, spreadsheets, and faxes. Staff rekeys the contents into core systems that were designed decades ago. Error rates stay stubbornly high because the process is manual by construction.

Then there is the data problem that predates every AI conversation. Most institutions run a core banking or policy administration system, a warehouse, a set of regional exceptions, and a graveyard of acquired platforms. Customer identity is fragmented across all of them. A question as simple as total exposure to one counterparty can take days to answer accurately.

Competitive dynamics make this worse rather than better. Customers now benchmark their bank against consumer apps, not against other banks. They expect instant decisions, instant disputes, and instant answers. Legacy institutions cannot deliver that on a manual operating model, which is exactly why more of them are starting this work with an AI consultancy engagement before committing to a build. That is the real problem AI is being asked to solve.

What AI Implementation in Financial Services Actually Involves

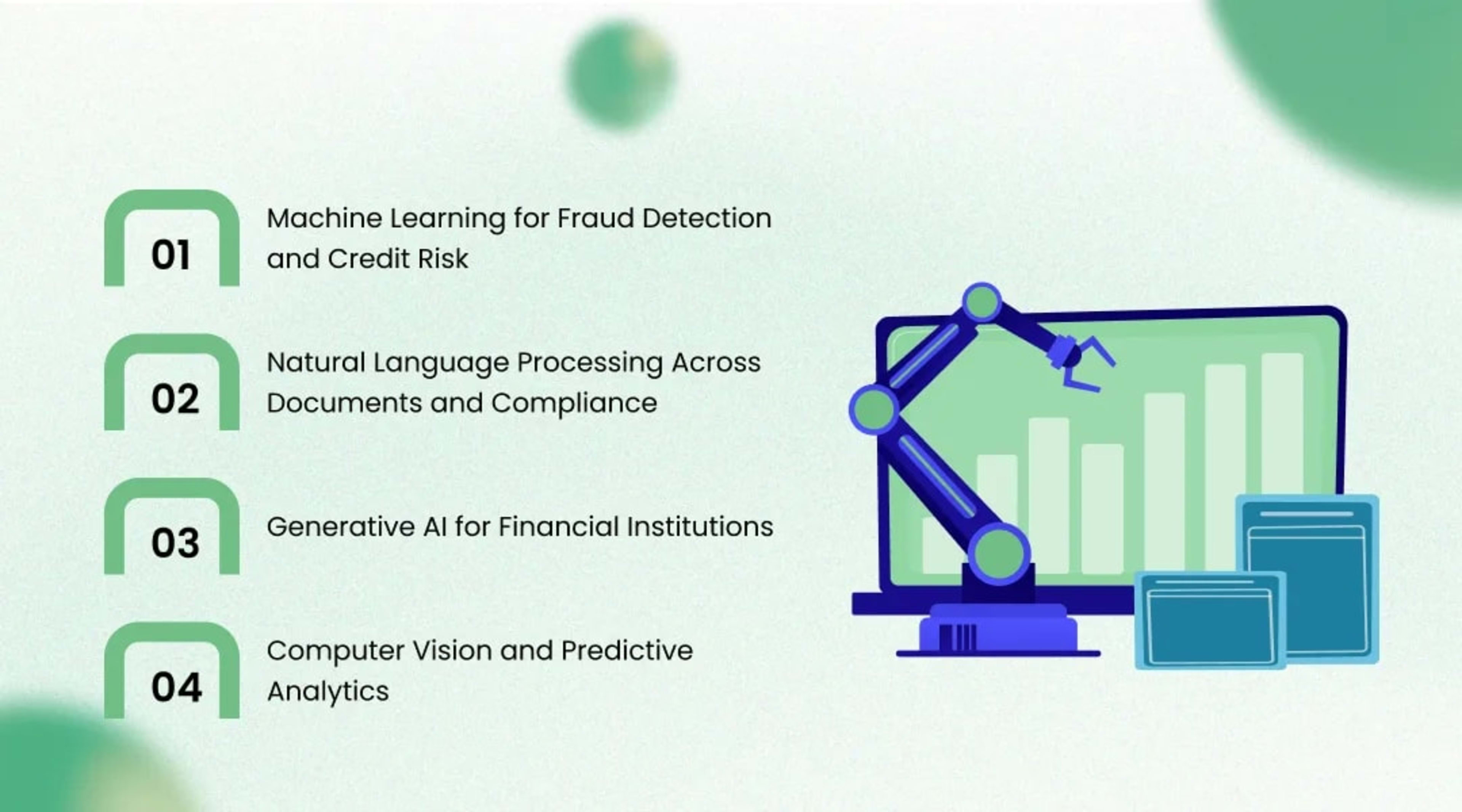

AI implementation in financial services is not one technology. There are four or five distinct technology families, each solving a different failure in the operating model. Vague talk about intelligence helps nobody. The useful exercise is mapping a specific technique to a specific broken process.

Machine Learning for Fraud Detection and Credit Risk

Machine learning fraud detection replaces static rules with models that score every transaction in milliseconds. Rules engines ask whether an amount exceeds a threshold in a suspicious country. Models ask whether this behaviour fits this customer at this hour on this device. Gradient-boosted trees and graph-based models now handle most production scoring at scale.

The graph piece matters more than most institutions realise. Fraud rings do not look unusual at the individual account level. They look unusual as a network of shared devices, addresses, and beneficiary accounts. Graph neural networks surface those rings by learning relationships rather than isolated features. This is where machine learning fraud detection consistently beats rules.

Credit risk uses the same machinery for a different question. Models ingest cash flow data, bureau records, transaction history, and behavioural signals. They produce probability of default estimates that adapt as conditions change. AI risk management in finance now extends the approach to early warning systems that flag deterioration months before a missed payment.

Natural Language Processing Across Documents and Compliance

Natural language processing attacks the document bottleneck directly. Intelligent document processing extracts structured fields from loan files, KYC packets, insurance claims, and trade confirmations. Modern systems combine layout-aware models with optical character recognition. Accuracy on standard forms routinely exceeds ninety-five percent with a human review queue for exceptions.

Compliance is the second natural home for NLP. Adverse media screening, sanctions name matching, and regulatory change tracking are all language problems. Entity resolution models decide whether the person in a news article is the same in the customer file. Doing this well cuts investigation time sharply.

Communications surveillance rounds out the picture. Banks must monitor trader chat, email, and voice for market abuse. Keyword lists produce noise. Language models trained on financial context understand intent, sarcasm, and coded speech far better, which is why KriraAI's work with banks and fintechs monitoring communications increasingly centres on domain-tuned models rather than generic ones.

Generative AI for Financial Institutions

Generative AI for financial institutions has found its footing in three places, not everywhere. The first is retrieval-grounded internal assistants. Relationship managers and contact centre agents ask questions in plain language. The system answers from policy documents, product terms, and account data with citations.

The second is drafting under supervision. Credit memos, suspicious activity report narratives, client review summaries, and audit responses are all structured writing tasks. A model produces the first version. A qualified human edits and signs it. That division of labour is what makes the deployment defensible.

The third is code and data work inside the institution. Legacy migration, test generation, and query writing all benefit from generative assistance. This is unglamorous, and it is where a great deal of the real value sits. KriraAI builds these production-grade assistant and workflow systems for enterprise clients, with the retrieval, evaluation, and audit layers that keep them safe in regulated environments.

Computer Vision and Predictive Analytics

Computer vision handles identity and physical evidence. Document liveness checks, face matching during onboarding, and cheque processing all run on vision models. Insurers use vision to estimate vehicle and property damage from photographs. Claims that once needed an adjuster visit can now be settled over the phone.

Predictive analytics covers the forecasting layer. Treasury teams predict intraday liquidity needs. Collections teams predict which delinquent accounts will self-cure. Marketing teams predict attrition before the customer closes the account. These are old statistical problems given new resolution.

The Quantified Business Impact of AI in Banking Operations

The honest answer is that returns cluster in a few places and disappoint elsewhere. AI in banking operations delivers its most reliable gains where volume is high, decisions are repetitive, and outcomes are measurable within weeks. Here is what institutions report when they measure properly.

Fraud and financial crime show the strongest numbers. Institutions replacing rules with hybrid model architectures commonly report false positive reductions between forty and sixty percent. Detection of previously missed fraud typically improves by twenty to thirty percent. The combined effect is fewer analysts clearing noise and fewer losses reaching the balance sheet, a pattern we unpacked in detail when looking at how banks use voice AI to catch fraud faster.

Document-heavy operations follow closely. Intelligent document processing in loan origination cuts manual handling time by fifty to seventy percent on standard files. Onboarding cycles that took nine days are compressed to two or three. Straight-through processing rates on retail applications climb into the seventies for institutions with clean data.

Contact centres show a more nuanced result. Deflection to self-service improves, but the bigger gain is agent handle time. Assistants that surface account context and next best action reduce average handle time by fifteen to twenty-five percent. First contact resolution improves because the agent stops searching across six systems.

Credit and collections produce the returns that reach the P and L fastest. Better risk ranking allows the same approval rate at lower loss, or a higher approval rate at constant loss. Institutions deploying early warning models report loss reductions in the range of ten to twenty percent on affected portfolios. Collections prioritisation lifts recovery rates by similar margins.

Developer productivity is the quiet winner. Engineering organisations using AI assistance report meaningful throughput gains on routine work. The effect is smaller than the vendor claims suggest. It is still real, and it compounds across a multi-year modernisation programme.

The pattern across all of these is worth stating plainly. Value concentrates where the process was already instrumented. If you cannot measure the baseline, you will not prove the gain.

Why Most Programmes Fail, and What the Turnarounds Did Differently

A widely cited finding across enterprise AI research is that the large majority of pilots never reach production. In financial services, the number is arguably worse because model risk governance adds a gate that most pilots were never designed to pass. Understanding the failure pattern is more useful than another success story.

Failed programmes share a signature. They start with the technology and hunt for a problem. They select use cases by executive enthusiasm rather than by process volume. They build on extracted data snapshots rather than live pipelines. Then they discover, at the end, that nobody owns the operational change.

Turnarounds share an equally consistent signature. They restart from a single process with a hard number attached. They fix the data pipeline before touching the model. They involve second-line risk from week one instead of week thirty. They ship a narrow capability into live operations and let it earn the right to expand.

The sequencing insight is counterintuitive. The teams that moved fastest overall were the ones that spent the first quarter on unglamorous foundations. Feature stores, entity resolution, lineage, and evaluation harnesses look like delays. They are the only reason the second and third use cases take weeks rather than years.

An Implementation Roadmap That Survives Contact With a Bank

A serious rollout runs in five stages. Each stage has an exit condition. Skipping a stage does not accelerate the programme; it relocates the failure to a later and more expensive point.

Run a readiness and value audit that inventories processes by volume, cost per unit, error rate, and data availability. Score each candidate on value and feasibility, then discard everything below the line.

Fix the data foundation for the two or three surviving candidates, including lineage, entity resolution, and access controls that satisfy your privacy obligations.

Build a pilot against a frozen baseline with a defined success metric, a control group where possible, and model risk sign-off designed in from the start.

Deploy narrowly into live operations with a human review queue, monitoring for drift, and a documented rollback path if performance degrades.

Scale horizontally by reusing the platform components rather than rebuilding, and retire the manual process only after the new one has run stably for a full cycle.

Governance runs alongside all five stages rather than after them. Model risk management frameworks in most jurisdictions already cover this territory. Treat your models as models, document assumptions, validate independently, and keep the challenger process alive. KriraAI works with enterprise teams to design this governance layer alongside the build, so that models reach production with validation evidence already assembled rather than reconstructed under audit pressure.

Talent structure deserves an explicit decision. The winning pattern is a small central platform team plus embedded practitioners in each business line. The central team owns tooling, evaluation, and standards. The embedded people own the problem and the change.

Common Mistakes and How to Avoid Them

Choosing use cases by novelty instead of by transaction volume, which guarantees a small numerator no matter how good the model becomes.

Measuring model accuracy instead of business outcome, the programme reports an F1 score while operations report no change in cost.

Treating the pilot data extract as the production pipeline, which turns deployment into a second full project nobody budgeted for.

Excluding compliance and model risk until the demo is complete, which converts a supportive function into a blocking one.

Automating a broken process rather than redesigning it, which produces the same bad outcome at higher speed.

Underinvesting in change management, so trained staff quietly revert to the old workflow within two months of launch.

Buying a platform before defining the problem, which anchors every future decision to a vendor roadmap you do not control.

The Challenges Nobody Should Minimise

Data quality remains the largest single obstacle, and it is not fixable by a model. Customer records are duplicated, addresses are inconsistent, and product hierarchies differ by region. Historical labels are frequently wrong, particularly in fraud, where confirmed outcomes lag by months. Training on bad labels produces confident errors.

Regulatory constraint is real, and it is tightening. Model explainability obligations in credit decisioning are not optional in most markets. The European AI Act classifies creditworthiness assessment and life insurance pricing as high risk, with documentation and oversight duties attached. Institutions operating across jurisdictions must satisfy the strictest applicable standard.

Talent scarcity compounds both problems. The people who understand both model behaviour and banking regulation are rare and expensive. Hiring them into a team with no platform means they spend their first year building plumbing. Retention suffers accordingly.

Integration complexity is the tax nobody prices correctly. Core systems expose limited interfaces and change slowly. Batch processing windows constrain what real-time actually means. Connecting a model to a mainframe-hosted product ledger is often harder than building the model.

Change management is the failure most frequently underestimated. A fraud analyst who has cleared alerts the same way for eleven years will not trust a score without explanation. If the interface does not show why, the analyst will investigate anyway. The efficiency gain evaporates.

Vendor concentration and cost drift deserve a mention too. Inference costs at production volume can surprise finance teams badly. Model versions change underneath you. Contracts that assume stable pricing and stable behaviour age poorly.

The Future of AI Risk Management in Finance and What Comes Next

Within three to five years, the durable change will be agentic workflow rather than single-point prediction. Today,y a model scores a transaction and hands it to a person. Tomorrow, a supervised agent will gather evidence, draft the disposition, and route only genuine ambiguity to a human. The human moves from processor to reviewer.

AI risk management in finance will shift from periodic to continuous. Credit reviews that happen annually will happen weekly against live cash flow data, a shift already underway for AI for finance and lending teams handling verification and EMI calls. Stress testing will run as an always-on simulation rather than a quarterly project. Early warning will become the default state of the portfolio.

Personalisation will finally get past the marketing layer. Products will be configured per customer within regulatory bands, not selected from a shelf of six. Pricing, limits, and terms will adjust dynamically to observed behaviour. This is where retail competition will be decided.

The regulatory environment will formalise around supervised autonomy. Expect explicit requirements for human accountability, audit trails of agent actions, and continuous validation evidence. Institutions that built governance early will absorb this cheaply. Those who bolted it on will rebuild.

Who gets left behind is predictable already. It will not be the institutions that move slowly on models. It will be the ones that never fixed their data. An institution with clean entity resolution and live pipelines can adopt any new technique in a quarter. An institution without them cannot adopt anything in a year.

Consolidation follows from that gap. Cost to serve will diverge sharply between the two groups. Mid-sized institutions on the wrong side will find their economics unworkable against digitally native competitors. Acquisition becomes the exit. This is why KriraAI focuses enterprise engagements on the foundational layer first, building the data, evaluation, and deployment infrastructure that makes every subsequent AI use case cheaper than the last.

Conclusion

Three points carry more weight than everything else in this analysis. First, value in financial services AI concentrates in high-volume, measurable, document-heavy, or decision-dense processes, and it largely evaporates elsewhere. Second, the constraint is rarely the model. It is data quality, integration, governance, and the willingness of experienced staff to change how they work. Third, the institutions that will look untouchable in five years are the ones spending this year on unglamorous foundations, because those foundations are what make every future capability cheap.

The uncomfortable implication is that most current activity is misdirected. Running twenty pilots is not a strategy. Picking two processes, instrumenting them properly, and shipping into live operations is a strategy. The gap between those two behaviours explains most of the variance in outcomes across the sector.

KriraAI works with banks, insurers, and financial technology firms to close exactly that gap, building production-grade AI systems with the data pipelines, evaluation harnesses, and governance evidence that regulated deployment demands. The engagements start with a value and readiness audit rather than a technology recommendation, because the sequencing decision matters more than the tooling decision. If you are trying to move a promising pilot into supervised production, or trying to work out which two processes deserve investment first, it is worth a conversation with the KriraAI team about what your data actually supports today.

FAQs

AI implementation in financial services means deploying machine learning, natural language processing, computer vision, and generative models into live financial workflows such as fraud detection, credit decisioning, compliance screening, and client servicing. Traditional automation follows explicit rules written by humans and behaves identically every time. AI systems learn statistical patterns from historical data and produce probabilistic outputs that adapt as conditions change. The practical difference is that rules break when fraudsters change tactics, while models retrain. The tradeoff is that AI systems require ongoing validation, monitoring for drift, and explainability evidence that rules never needed.

A first production deployment of AI in banking operations typically takes six to nine months at an institution with reasonable data foundations, and twelve to eighteen months at one without them. The model itself usually accounts for less than a quarter of that time. The majority goes to data pipeline construction, entity resolution, integration with core systems, model risk validation, and operational change management. Subsequent use cases move far faster, often reaching production in eight to twelve weeks, because platform components, governance templates, and evaluation harnesses already exist. This is why the first project should be chosen for foundational value rather than for speed.

Machine learning fraud detection consistently outperforms rules-based systems on both dimensions that matter. Institutions moving to hybrid architectures, where models score transactions and rules handle regulatory hard stops, commonly report false positive reductions of forty to sixty percent alongside detection improvements of twenty to thirty percent. The gain comes from modelling behaviour in context rather than testing fixed thresholds. Graph-based models add further lift by identifying fraud rings through shared devices, addresses, and beneficiaries that look unremarkable individually. Rules remain necessary for sanctions enforcement and explicit policy, so the correct architecture combines both rather than replacing one entirely.

Generative AI for financial institutions is safe in regulated processes when it operates under retrieval grounding and human sign-off rather than autonomously. The proven pattern restricts the model to answering from an approved document corpus with citations and requires a qualified employee to review and approve any output that reaches a customer or regulator. Suitable applications include drafting credit memos, summarising client reviews, writing suspicious activity report narratives, and answering internal policy questions. Unsuitable applications include unsupervised credit decisions and unreviewed customer communications. The governing controls are corpus curation, output evaluation, audit logging, and clear human accountability for every published artefact.

AI risk management in finance requires treating every deployed model as a governed asset under an existing model risk management framework. That means documented development standards, independent validation before deployment, defined performance thresholds, continuous monitoring for drift and bias, and a challenger model process. High-risk applications such as creditworthiness assessment carry additional obligations under regimes including the European AI Act, covering documentation, human oversight, and transparency to affected individuals. Practically, institutions should assign a named model owner, maintain lineage from raw data to decision, retain approval evidence, and rehearse a rollback path. Governance built during development costs a fraction of governance reconstructed during examination.

Ridham Chovatiya is the COO at KriraAI, driving operational excellence and scalable AI solutions. He specialises in building high-performance teams and delivering impactful, customer-centric technology strategies.